Published by

Internal audit is a critical safeguard for UK mid-market organisations. Yet most internal audit functions remain stubbornly manual, relying on statistical sampling and periodic testing cycles that capture only a fraction of transactions. The Financial Reporting Council (FRC) has made clear that audit committees must demonstrate robust oversight of the control environment. Meanwhile, regulatory expectations are tightening, and the cost of audit failure—reputational, legal, and financial—continues to climb.

Artificial intelligence is transforming how leading organisations approach internal audit and controls. Rather than sampling 5–15% of transactions, AI-powered continuous auditing platforms can now monitor 100% of activity in real time, flagging anomalies and control breaches within hours instead of weeks. The result is not just better governance; it is fundamentally different economics. Audit teams spend less time on routine testing and more time on strategic risk management. Fraud is detected faster. Control failures are remediated before they compound into material issues.

This article explores how AI is reshaping internal audit for UK mid-market firms, the business case for deployment, and the practical steps to implement continuous monitoring and anomaly detection in your organisation.

Key Takeaway

AI-powered continuous auditing transforms internal controls from a periodic, sample-based process into a real-time, comprehensive monitoring system. For UK mid-market organisations, this shift addresses the FRC's governance expectations, reduces audit cost per transaction, and enables audit teams to focus on high-risk areas and strategic value creation.

The Internal Audit Challenge for UK Mid-Market Firms

Most UK mid-market organisations operate internal audit functions that have changed little in two decades. Audit cycles are annual or semi-annual. Testing is performed on a small, statistically representative sample of transactions. Low-risk areas receive minimal attention. High-risk areas are revisited annually, and corrective action verification happens months after the original finding.

This model was designed for a slower-moving, less complex business environment. Today, mid-market firms face accelerating transaction volumes, increasingly complex supply chains, multi-jurisdictional regulatory requirements, and growing expectations from audit committees and the FRC about the governance of digital systems and data.

The FRC's updated UK Corporate Governance Code (2024) makes clear that audit committees must assess and report on "the effectiveness of the control environment." This language signals an expectation that audit is not purely compliance-focused, but actively demonstrates to investors and stakeholders that controls are working as designed. A manual, sample-based audit function struggles to provide that assurance with confidence.

Furthermore, the current approach is labour-intensive. Audit teams spend 40–60% of their time on routine, low-risk testing—work that adds little strategic value. Finding a qualified internal auditor is difficult; retaining them in a role that is often seen as administrative is harder still. As firms grow, audit headcount does not scale proportionally, creating a gap between audit scope and audit capacity.

How AI Transforms Internal Audit and Controls

Artificial intelligence transforms internal audit by automating the most time-consuming, repetitive tasks and extending audit coverage to previously untestable volumes of data.

Machine learning models can be trained to recognise patterns associated with control failures, fraud, and regulatory breaches. Once trained, these models run continuously, scanning 100% of transactions in real time—not a sample, not a monthly batch, but every transaction as it occurs. When a pattern is detected that deviates from the expected norm, the system flags it for human review within hours, not weeks.

This shift from periodic testing to continuous monitoring is fundamental. In a manual audit, a fraudulent supplier invoice might not be detected until the next audit cycle, six months later. By then, the fraud has compounded, control gaps may have been exploited systematically, and remediation is more difficult. An AI-powered system detects the same invoice anomaly within hours, enabling the business to act immediately.

The intelligence is not just technical; it is contextual. AI systems learn the normal patterns for each transaction type, each supplier, each cost centre. They account for seasonality, business cycles, and changes in organisational structure. A large purchase order that would be flagged as an anomaly in normal circumstances might be recognised as expected in the context of a major project or acquisition.

From Sample-Based to Continuous Auditing

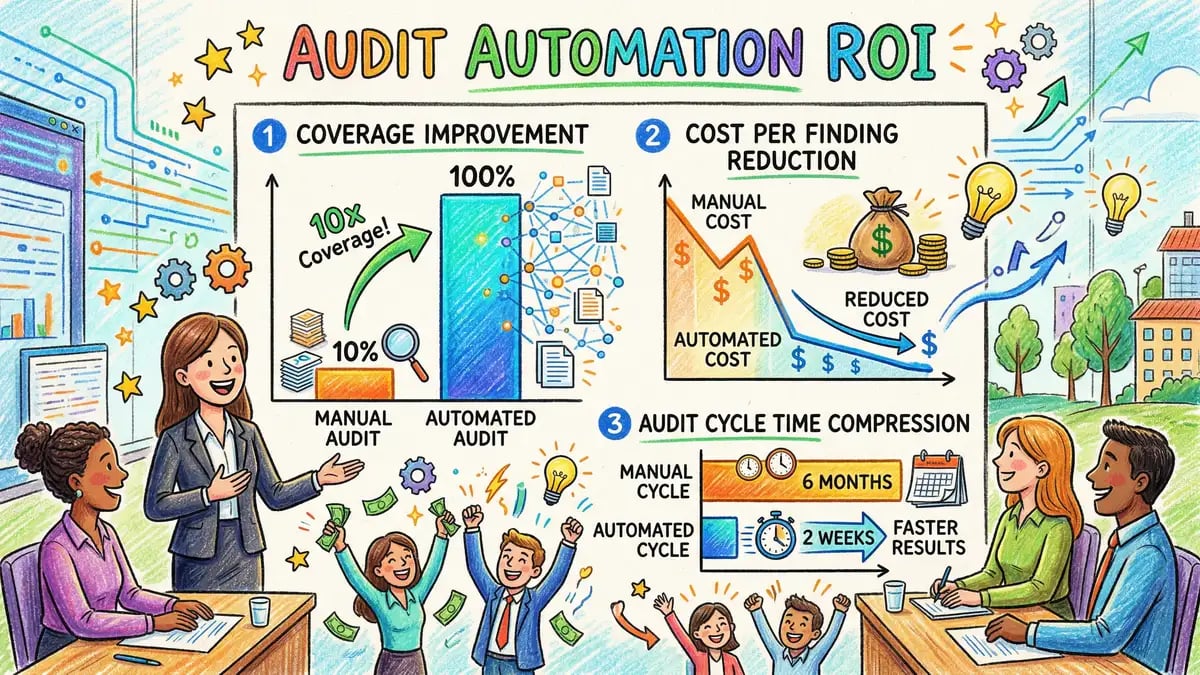

Traditional internal audit operates on a sampling methodology: test a statistically representative subset of transactions, infer control effectiveness across the population, and report results. For a portfolio of 10 million annual transactions, a sample of 100–500 transactions is considered statistically rigorous.

This approach made sense when testing costs were high and data processing was laborious. It no longer reflects the risk landscape. A control failure detected in 5% of transactions (or missed entirely if the sample was fortunate) can represent millions of pounds in undetected non-compliance or fraud.

Continuous auditing, powered by AI, inverts this logic. Testing costs fall dramatically—machines do the testing—so testing the entire population becomes economically feasible. The result is visibility and assurance previously impossible to achieve.

Consider accounts receivable. A manual audit might test 200 invoices from a population of 500,000. AI continuous auditing monitors all 500,000 transactions in real time, checking for:

- Duplicate billing

- Invoices billed but not delivered

- Unusual price variances

- Invoices outside normal payment terms

- Invoices to previously blacklisted or related-party suppliers

- Transactions that violate approval hierarchies or segregation of duties rules

Each rule can be refined with machine learning. Over time, the system learns which combinations of factors are predictive of genuine risk versus false positives, continuously improving accuracy.

AI-Powered Anomaly Detection and Fraud Prevention

Anomaly detection is the core capability of AI-powered audit. Machine learning models are trained on historical transaction data to learn the "normal" distribution of transactions. Once trained, the model identifies transactions or patterns that fall outside the expected range.

This is fundamentally different from rule-based auditing. A rule-based system checks: "Is the transaction above £100,000?" or "Is the supplier on the approved list?" These rules are brittle; they catch only what the auditor anticipated. Anomaly detection models catch the unexpected, the novel, the deviation—precisely where fraud and control failures often hide.

Fraud typically manifests as a pattern across multiple transactions. A fraudster might gradually inflate invoices from a supplier, or create a series of small transactions just below the approval threshold. A human auditor reviewing individual transactions would miss the pattern. An anomaly detection model, trained on months of historical data, identifies the emerging pattern immediately.

Leading audit technology platforms (TeamMate+, AuditBoard, HighBond, MindBridge) embed multiple anomaly detection techniques:

- Statistical anomaly detection: Identifies transactions that fall outside expected distributions (e.g., unusually high amounts, unusual timing)

- Isolation Forest and Clustering: Groups similar transactions and identifies isolates or clusters that deviate from the norm

- Network analysis: Maps relationships between suppliers, employees, and transactions to identify suspicious patterns

- Time-series analysis: Detects changes in patterns over time (e.g., a supplier's invoice amounts suddenly increasing)

The practical result is that organisations can detect fraud weeks or months earlier than with manual auditing. The Institute of Internal Auditors (IIA) reports that AI-assisted fraud detection reduces the time from fraud occurrence to discovery from an average of 14 months to under 3 months.

Automated Control Testing and Compliance Monitoring

Beyond anomaly detection, AI automates the routine, rules-based testing that consumes so much audit time.

Control testing typically checks whether key controls are operating. For example: "Are all supplier invoices authorised by a manager before payment?" "Are journal entries reviewed and approved?" "Are access rights reviewed quarterly?" In a manual audit, this testing is labour-intensive. The auditor reviews transaction logs, permission matrices, and approval records—work that is methodical but offers little intellectual challenge.

Audit platforms with AI can automate these tests. The platform reads from enterprise systems—the ERP system, the general ledger, the HR system—and verifies that controls operated as designed across 100% of transactions. The auditor no longer spends time on data gathering and validation. Instead, the auditor focuses on interpreting results, investigating root causes, and designing remediation.

Compliance monitoring benefits similarly. Many mid-market firms must comply with regulations such as the Bribery Act 2010, UK GDPR, FCA rules, or sector-specific requirements (e.g., Health and Safety at Work, or industry-specific environmental standards). Compliance with these rules often translates into control requirements: vendors must be screened against sanctions lists; employees must complete training; certain transactions must be approved; data processing must be logged.

AI automates these compliance checks. Has the new supplier been screened? Has the employee completed the required training? Is the transaction permissible under the GDPR? Is the data export within policy? Rather than manual spot-checking, the system checks 100% of applicable transactions continuously.

Audit Technology Platform Landscape for UK Firms

Several leading platforms serve the UK mid-market audit and internal controls market. Each offers varying combinations of workflow automation, continuous monitoring, anomaly detection, and integration.

TeamMate+ (Wolters Kluwer): A comprehensive audit management system with integrated continuous auditing and data analytics. TeamMate+ is strong on workflow automation and is widely used by larger audit functions. Pricing typically ranges from £15,000–£40,000 annually for mid-market deployments, depending on transaction volume and ERP system integrations.

AuditBoard: A modern, cloud-native platform focusing on integrated audit and risk management. AuditBoard offers strong anomaly detection and predictive analytics capabilities. The platform emphasises user experience and mobile accessibility. Pricing is typically £12,000–£35,000 annually for mid-market use.

Galvanize (Diligent): A broad governance, risk, and compliance (GRC) platform that includes audit and internal controls functionality. Galvanize is especially strong for organisations managing complex, multi-jurisdictional compliance. Pricing varies widely based on scope but typically starts at £15,000 annually.

HighBond (Unit4): Specialises in continuous auditing and data analytics. HighBond is particularly effective for organisations seeking to implement continuous monitoring and fraud detection at scale. Pricing typically ranges from £8,000–£30,000 annually, with lower pricing for organisations focused on analytics only.

MindBridge (part of Thomson Reuters): A newer entrant focused on AI-powered audit analytics and anomaly detection. MindBridge emphasises explainnable AI and ease of use for audit teams. Pricing is typically £10,000–£25,000 annually.

Caseware IDEA (part of Easyaudit Holdings): A long-established data analytics and continuous auditing platform. IDEA is especially popular in mid-sized audit teams. Pricing typically ranges from £5,000–£20,000 annually.

When selecting a platform, UK mid-market organisations should evaluate: (1) integration capabilities with existing ERP and financial systems (SAP, Oracle, Sage, Microsoft Dynamics); (2) support for continuous monitoring versus batch-based testing; (3) anomaly detection algorithms and customisation; (4) ease of use for audit staff (many are not data scientists); and (5) vendor stability and roadmap (the audit technology market is consolidating; several platforms have been acquired or are discontinuing).

UK Corporate Governance Code and Regulatory Drivers

The FRC's UK Corporate Governance Code, updated in 2024, strengthens expectations for audit committee effectiveness and the robustness of internal controls. Whilst the Code applies directly only to listed companies, its influence cascades through the mid-market: many private equity-backed firms must comply; many private companies voluntarily adopt code principles; and banks and lenders increasingly expect governance practices aligned with code expectations when assessing lending risk.

Key code expectations relevant to internal audit and controls include:

- Assessment of control environment: Audit committees must assess and report on whether "the management and the board have established appropriate and effective internal controls." This signals an expectation of evidence, not just assurance, that controls are working.

- Audit committee effectiveness: The code expects audit committees to have sufficient resources and expertise to hold management accountable for financial reporting and internal controls. This implies that audit functions must have adequate funding and tools to discharge their responsibilities credibly.

- Risk management: Boards must assess the effectiveness of risk management systems. Internal audit plays a critical role in providing evidence of whether key business and compliance risks are adequately controlled.

- Cyber security and data governance: The code increasingly emphasises cyber risk and data governance. Audit must be able to provide assurance over IT controls and data handling, which requires visibility into digital transactions and systems.

Beyond the FRC code, regulatory expectations are tightening across multiple domains. The International Audit and Assurance Standards Board (IAASB) continues to evolve audit standards toward greater use of data analytics. The Institute of Internal Auditors has issued guidance on the use of AI and automation in internal audit. Professional bodies including ICAEW and CIMA have published frameworks for audit committee effectiveness that increasingly reference the use of technology to enhance assurance.

For organisations subject to specific sector regulations (e.g., FCA rules for financial services, CQC inspections for healthcare), continuous monitoring of compliance often becomes an implicit expectation. Regulators increasingly expect organisations to be able to demonstrate real-time or near-real-time compliance evidence, not retrospective testing.

Implementation Roadmap for AI-Powered Audit

Implementing AI-powered continuous auditing is not a "big bang" project. Leading organisations adopt a staged approach, starting with high-risk, high-volume transaction streams and expanding gradually.

Stage 1: Pilot (Months 1–3)

Begin with a single, high-risk, high-volume process. Accounts payable is a common starting point: it is high-risk (fraud, unauthorised spend), high-volume (thousands of invoices annually), and well-understood by the finance team. Work with the platform vendor to ingest 12 months of historical AP transactions, define rule sets and anomaly thresholds, and run the system in "shadow mode"—monitoring and flagging anomalies but not blocking transactions.

The goal is to validate the system's accuracy and calibrate it to your organisation's environment. You will discover false positives and false negatives. You will learn that some "anomalies" flagged by the system are legitimate business events (e.g., a large year-end supplier payment is normal, not suspicious). By the end of the pilot, you will have a tuned model ready for operational use.

Stage 2: Operationalisation (Months 3–9)

Move the pilot process into production, with the system actively monitoring and flagging anomalies for review. Assign ownership: who reviews flagged transactions? Who determines whether a flag is a genuine issue or a false positive? Who initiates remediation or escalation? Document the review process and SLAs.

In parallel, expand to a second process. Accounts receivable is a logical next step (revenue fraud, credit risk). Payroll and expenses are also common candidates (ghost employees, inflated expense claims). The second implementation is typically faster than the first; you have learned how to configure the system, integrate data, and manage the workflow.

Stage 3: Expansion (Months 9–18)

Expand continuous monitoring to core financial processes: general ledger journals (detecting unauthorised or unusual journal entries), fixed asset transactions, intercompany transactions, and bank transactions. In parallel, layer in compliance monitoring for regulated processes: sanctions screening of new suppliers, employee conflicts of interest, GDPR data exports, and regulatory reporting.

Stage 4: Strategic Integration (Months 18+)

Mature use of the platform shifts from operational monitoring to strategic analytics. Use anomaly detection insights to inform audit planning. Use trend analysis to identify emerging risks. Use predictive analytics to forecast future control failures and resource audit activity accordingly. Integrate continuous audit findings into the audit committee reporting cycle, so governance gets real-time visibility into control health rather than annual snapshots.

Building the Business Case for Audit Automation

The financial case for AI-powered audit is compelling for mid-market organisations, though the timeline and magnitude of benefit vary by company size and audit maturity.

Cost Savings: The largest benefit is labour efficiency. Audit teams currently spend 40–60% of time on routine, low-risk testing. A mid-size audit team (4–6 people, costing £300,000–£450,000 annually) can redeploy 40–60% of that capacity—£120,000–£270,000 of effort—to higher-value audit activities or risk management. In some cases, this enables the audit team to take on expanded scope (e.g., continuous IT audit, cybersecurity audit) without increasing headcount.

Additionally, continuous monitoring reduces the cost per transaction audited. With manual sampling, the cost to test one transaction might be £50–£100 (auditor time divided by number of transactions tested). With continuous monitoring, the cost is fixed (the platform cost, £10,000–£40,000 annually, divided by the number of transactions monitored). For an organisation with 5 million annual transactions, continuous monitoring costs approximately £0.002–£0.008 per transaction, versus £50–£100 per transaction for manual testing.

Risk Reduction: Earlier fraud detection reduces financial loss. Research from audit technology vendors and the Association of Chartered Certified Accountants (ACCA) demonstrates that organisations with mature continuous audit programmes detect fraud 11 months earlier than organisations relying on manual audit, reducing average fraud loss per incident by approximately 30%. For organisations with even modest fraud risk (e.g., a 2–3% error rate in high-risk processes), the reduction in losses can exceed the platform cost within the first year.

Governance and Regulatory Benefits: Better assurance over controls reduces regulatory risk and audit committee concern. This is difficult to quantify but has real value: audit committees feel more confident in reported financial results; external auditors may reduce substantive testing if they see evidence of robust continuous audit controls (potentially reducing external audit fees); and regulatory inspections are more likely to view the organisation favourably if governance practices are demonstrably robust.

Typical ROI Timeline: For mid-market organisations, ROI is typically achieved within 18–24 months. Year 1 costs include the platform (£10,000–£40,000), implementation and integration (£20,000–£60,000), and training. Year 1 benefits include labour efficiency and modest fraud detection benefits. By Year 2, labour redeployment is fully realised, and fraud detection benefits compound. By Year 3, the platform is mature and fully optimised, and the annual recurring cost becomes very attractive.

Common Implementation Challenges and Solutions

Most organisations underestimate the data integration complexity of continuous audit. Here are the most common challenges and solutions:

Challenge: Data Extraction and Integration

Audit platforms must read from ERP systems, general ledgers, HR systems, and sometimes legacy or departmental systems. Many UK mid-market firms run multiple systems that do not integrate seamlessly. Extracting data reliably, in the right format, and on schedule requires skilled technical resources.

Solution: Invest in data integration upfront. Engage either the platform vendor's professional services team or a systems integrator experienced in audit data integration (firms like Deloitte, PwC, and specialist integrators like Chariots and Objectwise offer these services). Use an integration platform-as-a-service (iPaaS) tool like Talend or Informatica to automate data flows and reduce ongoing manual effort.

Challenge: Defining Rules and Thresholds

Audit teams often struggle to translate business risk into rules and anomaly thresholds. What constitutes a "suspicious" supplier invoice? What is the right fraud detection threshold? Setting thresholds too high results in missed risks; too low results in alert fatigue and wasted time on false positives.

Solution: Involve both the audit team and process owners (e.g., the AP team for supplier invoice rules) in threshold definition. Start conservatively and tune over time. Use the "shadow mode" pilot phase to test rules without enforcement, calibrate based on real data, and then move to production with confidence.

Challenge: Organisational Resistance

Business process owners sometimes view continuous audit as threatening. "Will the system flag my decisions?" "Will I be blamed for anomalies?" This perception can undermine adoption.

Solution: Communicate the purpose clearly: continuous audit is designed to catch systemic control failures and fraud, not to police individual decisions. Train process owners on how the system works and how to interpret alerts. Early wins help; when the system identifies a genuine fraud or control failure that manual audit would have missed, support for the system typically increases dramatically.

Challenge: Scaling Across the Organisation

Many organisations deploy continuous audit to finance initially, then struggle to extend it to other departments (HR, procurement, operations). Each department has different data sources, different process risks, and different readiness.

Solution: Prioritise based on risk and readiness. Finance and supply chain often have the clearest data and highest risk; HR and operations may require more work. Plan for 6–9 months per major process area, and manage change actively, including training and stakeholder communication.

Frequently Asked Questions

What is the difference between continuous auditing and continuous monitoring?

The terms are sometimes used interchangeably, but there is a distinction. Continuous monitoring refers to the business's own monitoring of its processes—e.g., a manager reviewing transaction exceptions. Continuous auditing refers to audit's use of automated tools to assess control effectiveness continuously. In practice, effective continuous auditing often leverages continuous monitoring data.

Do we need to replace our current audit platform to implement AI audit?

Not necessarily. Some audit platforms (TeamMate+, AuditBoard) have embedded AI and continuous audit capabilities. Others (e.g., legacy audit software) do not. If your current platform lacks these capabilities, you have two options: (1) upgrade to a modern platform, or (2) adopt a best-of-breed continuous audit tool (like HighBond or MindBridge) that integrates with your existing platform. Option 2 is increasingly popular for organisations with significant investment in their current platform.

How much historical data do we need to train AI models?

Typically, 12 months of historical transaction data is sufficient for anomaly detection models to establish a baseline and begin flagging anomalies with reasonable accuracy. However, 24 months is better, especially for seasonal processes (e.g., year-end accruals, holiday expenses, seasonal purchasing). If your organisation has experienced significant changes in the past 12–24 months (e.g., acquisition, major process change, pandemic-related disruption), be cautious: the AI model will be trained on an unrepresentative baseline.

What is the typical time to implement continuous audit?

A pilot for a single high-volume process (e.g., accounts payable) typically takes 8–12 weeks: data integration (3–4 weeks), rule definition and testing (2–3 weeks), and shadow mode calibration (2–4 weeks). Expanding to additional processes is typically faster. A full rollout across multiple core financial processes (AP, AR, payroll, GL, fixed assets) typically takes 9–18 months.

Do we need specialist AI or data science skills?

Ideally, yes. However, most modern audit platforms are designed to be used by audit professionals, not data scientists. The platform vendors provide training and support for configuration and interpretation. That said, for sophisticated anomaly detection tuning and custom machine learning models, having a data analyst or data scientist on staff (or available through a partner) is helpful.

How does continuous audit affect external audit?

External auditors are increasingly interested in organisations' continuous audit capabilities. If a client demonstrates robust continuous monitoring of accounts payable, for example, the external auditor can reduce substantive testing of AP transactions, potentially reducing external audit fees. Conversely, if continuous audit reveals control gaps, external auditors may increase testing. Overall, transparency about audit controls typically benefits external audit relationships and may reduce external audit cost.

Related Reading

To deepen your understanding of AI in finance and internal controls, explore these complementary topics:

- AI for Finance and Accounting — The broader context for AI-powered internal controls, including financial planning, reporting, and operational finance.

- AI for Accounting — How AI is transforming core accounting processes, from data entry to reconciliation and financial close.

- AI for Accounts Payable — A deep dive into invoice processing, three-way matching, and fraud detection in supplier payments.

- AI for Financial Forecasting — Using machine learning and predictive analytics to improve budgeting and financial planning accuracy.

- AI for Expense Management — Automating employee expense reporting, detecting non-compliant claims, and improving policy compliance.

- AI for Regulatory Reporting — Ensuring accuracy and timeliness in regulatory filings using AI-powered data gathering and validation.

- AI for Treasury Operations — Cash management, liquidity forecasting, and counterparty risk management with AI.

- AI Governance Framework — Establishing governance structures to oversee AI deployment and ensure responsible use of automation.

- AI and Compliance in Regulated Industries — Navigating regulatory expectations around AI use and maintaining audit trails for auditor and regulator scrutiny.

Conclusion: The Future of Audit is Continuous

Internal audit is at an inflection point. The traditional model—periodic testing of statistically representative samples—is giving way to continuous, AI-powered monitoring of entire transaction populations. For UK mid-market organisations, this shift is not optional; it is increasingly essential to meet governance expectations, manage fraud risk, and deploy audit resources efficiently.

The business case is clear: labour efficiency, fraud detection, and better governance risk management combine to deliver ROI within 18–24 months. The platforms are mature and proven. The barriers to adoption are primarily organisational and technical, not fundamental limitations of the technology.

The key decisions are when to start and what processes to prioritise. Most organisations that have implemented continuous audit report that they wish they had started sooner. The longer you wait, the further you lag peers in governance maturity and the more fraud risk you carry unnecessarily.

Ready to Transform Your Internal Audit?

Helium42 helps UK mid-market organisations design and implement AI-powered audit and internal controls programmes. From platform selection through full deployment, we guide every step of the journey.